Now that I nailed my life after reaching financial independence, here are some numbers to back it up. As I previously stated:

Early retirement for me means to have my basic monthly expenses of €1000 covered for the rest of my life.

I need to develop an investment which yields €1K monthly (or €12K yearly) continuously for the rest of my life. I will live out of the interest and never have to withdraw from the main capital.

This yearly income for me will come from a combination of real estate and stock market investments. I will have additional income from side hustles but I don’t really know how much to expect from a side hustle. I consider this income a bonus and I don’t count it in the early retirement calculations.

How much do I need to reach financial independence?

The big question comes – how much do I need to save and invest before I can reach my goal? I will use the 4 Percent Rule to determine how much I can withdraw from a retirement account each year.

I need to have €300K in investments which will yield €12K (or 4%) yearly.

This rule seeks to provide a steady stream of funds, while also keeping an account balance that allows funds to be withdrawn for a number of years. The 4% rate is considered a “safe” rate, with the withdrawals consisting primarily of interest and dividends.

How will I do this in 5 years?!

The financial independence goal is something I have been working on for a while. I have been saving and investing, and I already have one-third of the €300K in various investments.

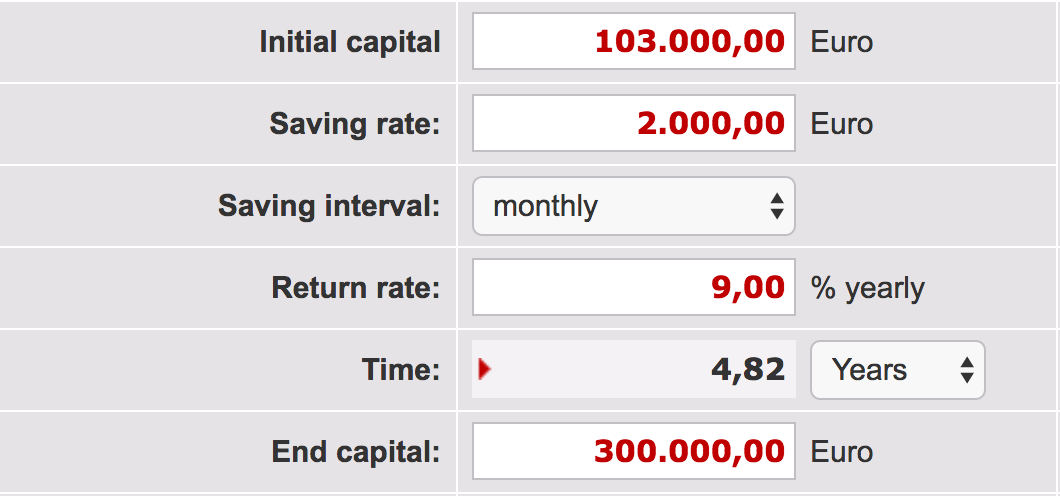

Using any compound interest calculator* online, here is the calculation I reached based on:

- Initial capital: €103K

- Annual return rate: 9% (in the last 26 years, DAX ETF has an average yearly return rate of 9%. This compares with around 10,1% for the S&P 500)

How many years I need to reach early retirement

This means that in order to reach €300K, I will need to save €2K every month for 4 years and 10months.

Saving €2K a month is a very, very, very steep goal. I still want to go on trips and will have unexpected emergencies. What if I save €1K monthly? Due to the power of the compound interest, I will need less than 7 years to reach my goal. I can live with that …

All the numbers are approximate but they give an idea of the direction I am aiming at.

Assumptions & Risks

The plan is not bullet proof and I have made some major assumptions. I am aware of these and ready to adjust the plan as I go. Here are some of the assumptions and risks:

- The return rate on my investments will be 9% yearly. It’s a well-known mistake to judge an investment on past performance. But I am in this for the long run.

Even there is a major stock market crash, I will buy even more of the ‘cheap’ shares and ETFs, as I still have the time to wait for the market to recover. Even if a crash happens in the fifth year, and my investment portfolio sinks, I will have to work for another couple of years until it rises again. - I have been on a simple living quest for a couple of years now. I believe I will continue decreasing my expenses. This might mean moving to low-expense country, home sitting, or taking more advantage of the shared economy (accommodation, transportation, etc.)

- I will greatly benefit from the compound interest on my current investments. It’s a well-known phenomenon – if I reinvest the yearly interest, the next year I will receive an interest on my bulk sum + the interest of year 1. Spread this over a long period of time, and the growth is exponential.

- I will have a steady source of income all these 5 years. I have marketable skills, which I continuously develop. So far I have never had trouble finding good employment.

- I will be growing my side hustles all this time. The inflow coming from side jobs will grow and I will be able to save and invest even more every month.

- There won’t be any major health emergency for me or my family during the 5 years. I will be able to work healthily, happily and productively.

- I will continue developing my investment and financial literacy and I won’t lose big amounts of money in riskier investments.

- I won’t make any major purchases such as a car, an apartment or a vacation home.

Conclusion

With all that being said, I am very confident that I will reach financial independence in the next 5 to 7 years. Only time will show, but the odds are in my favor.

Even if I don’t reach the goal by Jan 2022, I will be on a very good way there. Even if it takes me a few more years – well, I will still have built a great foundation.

Now it’s your turn! Do you see any cracks in my plan? Let me know in the comments section below!

******

* I use this Sparrechner calculator which is very good but it’s in German. You can search for ‘compound interest calculator’ or use this calculator in English.

******

Update, 31st July 2017:

After completing a 6-month sabbatical as a test-drive of my financial independence goal, I realized that the goal is twice as far as I thought.

€1K monthly is indeed what I need to physically survive. But if I want to live a good life beyond the basics, I would need at least twice as much before I can announce financial independence.

******

I have a question about the initial capital of 103K, where did that come from/how long it took?

Hi there!

The initial capital is a combination of my savings and a small inheritance – my networth 2years ago (2017).

I’m in my mid 30s now so it took about 15years – since I have an income of my own.